审计英语

1.

注册会计师在审计ABC公司时,使用PPS抽样方法测试ABC公司2012年12月31日的应收账款余额。2012年12月31日ABC公司的应收账款账户余额为6 000 000元。注册会计师确定的可接受误受风险为5%,可容忍错报为120 000元,预计总体错报为30 000元。拟测试的应收账款明细账户有100 000个。注册会计师在选取样本时采用系统选样法。假设:在样本中发现了2个错报。第一个账面金额为2 000元的项目有500元的高估错报,第二个账面金额为3 000元的项目有1 500元的高估错报。

附:PPS抽样风险系数表(适用于高估)

高估错报数量误受风险

1% 5% 10% 15%

0 4.61 3.00 2.31 1.90

1 6.64 4.75 3.69 3.38

2 8.41 6.30 5.3

3 4.72

3 10.05 7.76 6.69 6.02

4 11.61 9.16 8.00 7.27

5 13.11 10.52 9.28 8.50

6 14.5

7 11.85 10.54 9.71

预计总体错报的扩张系数表

误受风险

1% 5% 10% 15% 20% 25% 30% 37% 50% 扩张系

1.9 1.6 1.5 1.4 1.3 1.25 1.2 1.15 1.0

数

<1> 、计算样本规模。

<2> 、计算总体错报上限。

<3> 、代注册会计师作出相关的审计结论。

<1>、

【正确答案】样本规模=(总体账面价值×风险系数)/[可容忍错报-(预计总体错报×扩张系数)]

=(6 000 000×3.00)/(120 000-30 000×1.6)=250

Sample size=(The carrying value of population×Risk coefficient)/[Tolerable misstatement-(Expected misstatement on population ×Expansion factor)]

=(6 000 000×3.00)/(120 000-30 000×1.6)=250

【答案解析】

【答疑编号10585766】

<2>、

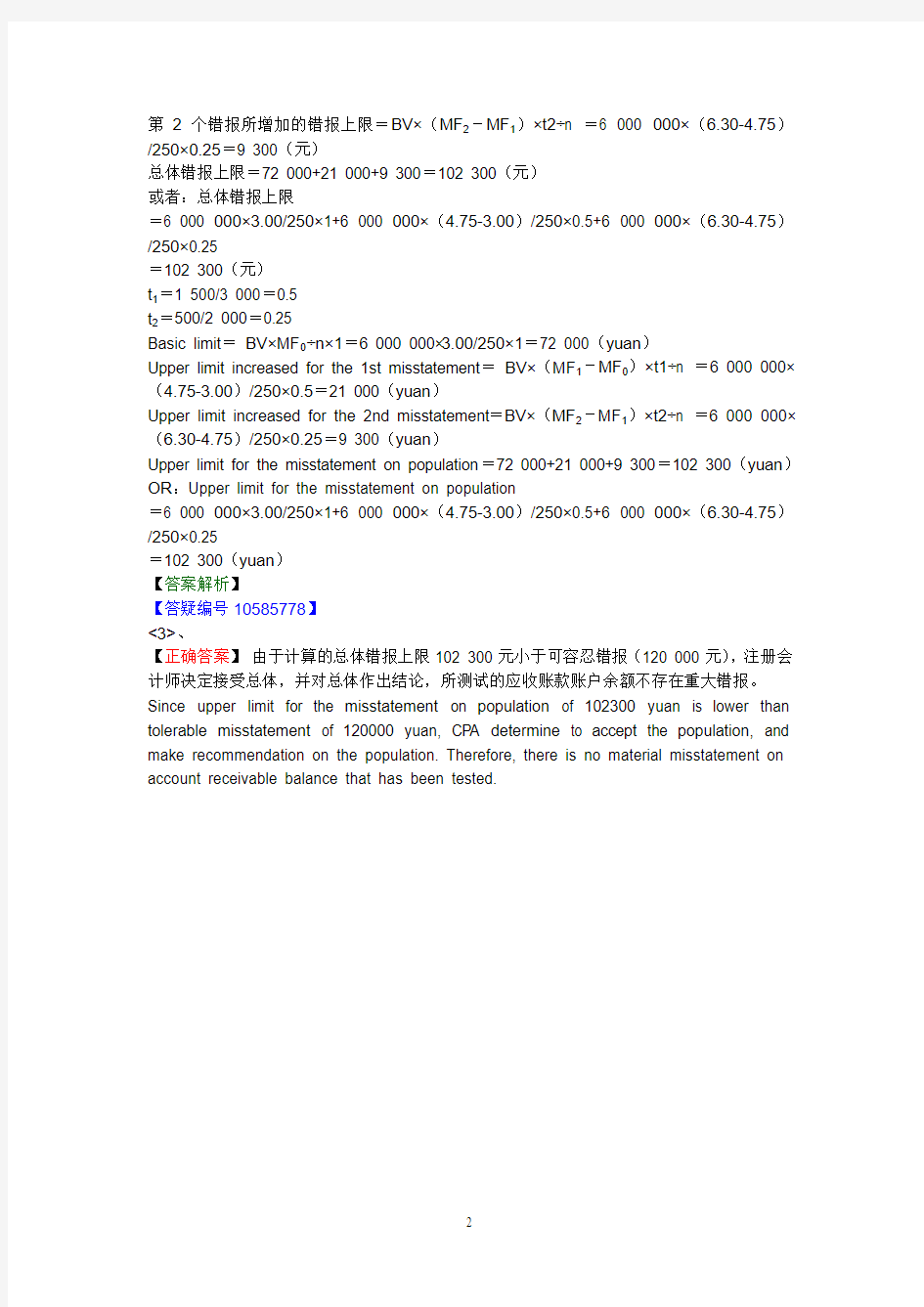

【正确答案】t1=1 500/3 000=0.5

t2=500/2 000=0.25

基本界限=BV×MF0÷n×1=6 000 000×3.00/250×1=72 000(元)

第1个错报所增加的错报上限=BV×(MF1-MF0)×t1÷n =6 000 000×(4.75-3.00)/250×0.5=21 000(元)

第2个错报所增加的错报上限=BV×(MF2-MF1)×t2÷n =6 000 000×(6.30-4.75)/250×0.25=9 300(元)

总体错报上限=72 000+21 000+9 300=102 300(元)

或者:总体错报上限

=6 000 000×3.00/250×1+6 000 000×(4.75-3.00)/250×0.5+6 000 000×(6.30-4.75)/250×0.25

=102 300(元)

t1=1 500/3 000=0.5

t2=500/2 000=0.25

Basic limit=BV×MF0÷n×1=6 000 000×3.00/250×1=72 000(yuan)

Upper limit increased for the 1st misstatement=BV×(MF1-MF0)×t1÷n =6 000 000×(4.75-3.00)/250×0.5=21 000(yuan)

Upper limit increased for the 2nd misstatement=BV×(MF2-MF1)×t2÷n =6 000 000×(6.30-4.75)/250×0.25=9 300(yuan)

Upper limit for the misstatement on population=72 000+21 000+9 300=102 300(yuan)OR:Upper limit for the misstatement on population

=6 000 000×3.00/250×1+6 000 000×(4.75-3.00)/250×0.5+6 000 000×(6.30-4.75)/250×0.25

=102 300(yuan)

【答案解析】

【答疑编号10585778】

<3>、

【正确答案】由于计算的总体错报上限102 300元小于可容忍错报(120 000元),注册会计师决定接受总体,并对总体作出结论,所测试的应收账款账户余额不存在重大错报。Since upper limit for the misstatement on population of 102300 yuan is lower than tolerable misstatement of 120000 yuan, CPA determine to accept the population, and make recommendation on the population. Therefore, there is no material misstatement on account receivable balance that has been tested.

2.

2012年10月,法天会计师事务所首次接受委托审计密云葡萄加工有限公司(以下简称密云葡萄)2012年度财务报表,委派注册会计师吕晓担任项目合伙人。密云葡萄为葡萄汁生产企业,2012年期初、期末存货余额占资产总额比重分别为65%和68%。存货主要包括葡萄和桶装葡萄汁,其中葡萄贮存在各采购地20个简易棚内,桶装葡萄汁贮存在密云葡萄的1个仓库内。密云葡萄对存货采用永续盘存制核算。密云葡萄拟于2012年12月31日起开始盘点存货,盘点工作由熟悉相关业务且具有独立性的人员执行。吕晓编制的存货监盘计划摘录如下:

(1)与存货相关的内部控制比较有效,加之存货单位价值不高,将存货认定层次重大错报风险评估为低水平。

(2)在对桶装葡萄汁实施监盘程序时,采用观察以及检查相关的收、发、存凭证和记录的方法,确定存货的数量。

(3)密云葡萄对葡萄的盘点计划是:2012年12月31日盘点12个简易棚内葡萄,2013年1月10日盘点其他8个简易棚内葡萄。吕晓根据密云葡萄的盘点计划,要求项目组成员在上述时间对葡萄实施监盘程序。

<1> 、根据审计准则的要求,指出注册会计师吕晓针对存货期初余额应当实施哪些审计程序。

<2> 、针对上述存货监盘计划第(1)项至第(3)项,逐项判断存货监盘计划是否存在缺陷。如果存在缺陷,简要提出改进建议。

<1>、

【正确答案】注册会计师吕晓针对存货期初余额实施的审计程序:监盘当前的存货数量并调节至期初存货数量;对期初存货项目的计价实施审计程序;对毛利和存货截止实施审计程序。

CPA Lu Xiao performs audit procedures as to opening balance of inventory: supervision the quantities of the inventory counted in current period, adjusting it to the opening inventory quantities; performing audit procedures on the valuation of opening inventories; performing audit procedures on gross profits and inventory cut-off.

【答案解析】

【答疑编号10585962】

<2>、

【正确答案】监盘计划(1)存在缺陷。

建议:将认定层次的重大错报风险评估为高水平,重点关注葡萄储存的相关控制以及质量状况。

监盘计划(2)存在缺陷。

建议:应当使用容器进行监盘或通过预先编号的清单列表加以确定;使用浸蘸、测量棒、工程报告以及依赖永续存货记录;选择样品进行化验与分析,或利用专家的工作。

监盘计划(3)存在缺陷。

建议:提请密云葡萄管理层同时盘点20个简易棚内的葡萄,注册会计师同时执行监盘程序。It has defect in plan (1) of supervision of inventory count

Recommendation: The estimated risk of material misstatement at assertion level should

be high, while mainly focusing on the relevant control and quality conditions of grape storage.

It has defects in plan (2) of supervision of inventory count.

Recomme ndation: Containers should be used in the process of the auditor’s attendance at inventory count, or it can be determined by the pre-numbered lists. It is suggested to use dipping, measuring rods, engineering reports and the perpetual inventory records; to assay and analyze the chosen samples, or to use the work of experts.

It has defects in plan (3) of supervision of inventory count.

Recommendation: Draw Miyun grape management attention to count grape in 20 sheds, at the same time CPA supervise the counting process.

3.

Y注册会计师负责对X公司2012年度财务报表进行审计。

<1> 、假定X公司存在财务报表层次重大错报风险,作为审计项目合伙人,Y注册会计师应当考虑采取哪些总体应对措施?

<2> 、假定评估的X公司财务报表层次重大错报风险属于高风险水平,指出Y注册会计师拟实施进一步审计程序的总体方案更倾向于何种方案?

<3> 、针对评估的财务报表层次重大错报风险,在选择进一步审计程序时,Y注册会计师可以通过哪些方式提高审计程序的不可预见性?

<4> 、假定X公司2012年度财务报表存在舞弊导致的认定层次重大错报风险,Y注册会计师应当考虑采用哪些方式予以应对?

<1>、

【正确答案】如果X公司存在财务报表层次重大错报风险,注册会计师应该实施下列总体应对措施:

①向项目组强调保持职业怀疑的必要性;

②指派更有经验或具有特殊技能的审计人员,或利用专家的工作;

③提供更多的督导;

④在选择拟实施的进一步审计程序时融入更多不可预见的因素;

⑤对拟实施的审计程序的性质、时间安排和范围作出总体修改。

If there are risks of material misstatement exist on Company X’s financial statement level, CPA should carry out the following overall measures:

① Emphasize on the necessity of maintaining professional skepticism;

② Assigns audit members with more experience and special skills and uses the work of experts;

③ Provides more assistance and guidance;

④ When choosing to implement further audit procedures, more unpredictable factors are included;

⑤ The nature, timing and extent of the audit procedures drafted to implement should be modified wholly.

【答案解析】

【答疑编号10586282】

<2>、

【正确答案】如果评估的X公司财务报表层次重大错报风险属于高风险水平,则Y注册会计师拟实施的进一步审计程序的总体方案通常更倾向于实质性方案。

If the risk of material misstatement on financial statement level of Company X evaluated is high, the overall strategy of drafted further procedures implemented by CPA Y usually tends to be substantive methods.

【答案解析】

【答疑编号10586283】

<3>、

【正确答案】针对评估的财务报表层次重大错报风险,在选择进一步审计程序时,Y注册会计师可以通过下列方式提高审计程序的不可预见性:

①对某些以前未测试过的低于设定的重要性水平或风险较小的账户余额和认定实施实质性程序;

②调整实施审计程序的时间,使其超出X公司的预期;

③采取不同的审计抽样方法,使当年抽取的测试样本与以前有所不同;

④选取不同的地点实施审计程序,或预先不告知X公司所选定的测试地点。

For the risks of material misstatement on financial statement level being evaluated, when choosing further audit procedures, CPA Y could improve the unpredictability of audit procedures in the following ways:

① For some previously untested and below the materiality level set or less risk of account balances and assertions, the implementation of substantive procedures should be made;

② Adjusting the timing of audit procedures being carried out to make it beyond Company X’s expectation;

③Adopting different audit sampling methods to make the samples selected in current year different from those in prior years;

④ Choosing different locations to perform audit procedures or not telling Company X the test location chosen in advance.

【答案解析】

【答疑编号10586284】

<4>、

【正确答案】如果X公司2012年度财务报表存在舞弊导致的认定层次重大错报风险,Y 注册会计师应当考虑采取下列方式予以应对:

①改变拟实施审计程序的性质,以获取更为可靠、相关的审计证据,或获取其他佐证性信息,包括更加重视实地观察和检查,在实施函证程序时改变常规函证内容,询问X公司的非财务人员等;

②改变实质性程序的时间,包括在期末或接近期末实施实质性程序,或针对本期较早时间发生的交易事项或贯穿于整个本期的交易事项实施测试;

③改变审计程序的范围,包括扩大样本规模,采用更详细的数据实施分析程序等。

If the risks of material misstatement on assertion level occur due to fraud exists in financial statement, CPA Y should consider the following methods:

① Change the nature of the audit procedures drafted to be implemented to obtain more reliable and relevant audit evidence or obtain other corroboration information, including more emphasis on physical observation and inspection, change the normal content of the confirmation in confirmation process, inquiring Company X’s non-financial personnel;

②Change the timing of the substantive audit procedures, including substantive procedures should be performed at or near the end of the year or perform tests on those transactions occurred at earlier time or occurred throughout the current period;

③Change the extent of audit procedures, including enlarge sample size, perform analytical procedures using detailed data.

4.

ABC会计师事务所接受委托对乙公司2012年度财务报表进行审计,A注册会计师担任审计项目合伙人。乙公司为孕婴服装加工企业,仓库中现有存货主要包括各种孕妇装、婴儿装、布匹、羊毛、棉线和各种辅助材料。为了保护宝宝的皮肤,推出更适合婴儿爬行的爬服,乙公司于2012年12月31日从杭州定制了一批柔软的面料,该材料由乙公司负责运输,截至盘点日货物尚在运输途中。乙公司在2013年1月8日对存货实施盘点,A注册会计师于同日实施存货监盘程序,有关部分监盘计划和监盘工作如下:

针对上述监盘计划和监盘工作有无不妥当之处?如有,请简述理由。

<1> 、存货监盘目标:检查乙公司2012年12月31日存货数量是否真实完整。

<2> 、存货监盘范围及时间安排:2013年1月8日对乙公司仓库库存的所有存货实施监盘。

<3> 、注册会计师在制定存货监盘计划时与乙公司沟通确定存货检查重点。

<4> 、在检查存货盘点结果时,注册会计师仅从存货实物中选取项目追查至存货盘点记录,目的是测试存货盘点记录的准确性和完整性。

<5> 、观察管理层制定的盘点程序的执行情况,对于正在加工中的存货,应当获取资产负债表日前后存货收发及移动的凭证,检查库存记录与会计记录期末截止的正确性。

<6> 、对实施抽盘程序发现的盘盈或盘亏的存货,由仓库保管员将存货实物数量和仓库存货记录调节相符。

<7> 、存货监盘结束时的工作。在乙公司存货盘点结束前,注册会计师还应当再次观察盘点现场,并取得和检查已填用、作废及未使用盘点表单的号码记录,不再实施其他审计程序,进一步确定盘点范围是否正确以及复核存货盘点结果汇总记录并评估是否正确反映实际盘点结果。

<1>、

【正确答案】不妥当。

理由:存货监盘的目标应该是获取乙公司2012年12月31日有关存货的存在和状况的审计证据,检查存货的数量是否真实完整,是否归属乙公司,存货有无毁损、陈旧、残次和短缺等状况。

Inappropriate.

Reason: The objectives of supervision of inventory counting are to obtain audit evidences relating to the existence and condition of Company Yi’s inventories on 31 December 2012, inspect the completeness of inventory quantities, identify whether the inventories are owned by Company Yi, whether the inventories are in the condition of damage, obsolescence, scrap and shortage.

【答案解析】

【答疑编号10585831】

<2>、

【正确答案】不妥当。

理由:存货监盘的范围不仅仅包括仓库库存的所有存货,还应该包括乙公司在途存货。Inappropriate.

Reason: The scope of supervision of inventory counting does not merely include all the inventories stored in warehouse, inventories in transit should also be included.

【答案解析】

【答疑编号10585834】

<3>、

【正确答案】不妥当。

理由:为了有效地实施存货监盘,注册会计师应与被审计单位就有关问题达成一致意见,但注册会计师应尽可能地避免被审计单位了解自己将抽取测试的存货项目。Inappropriate.

Reason: In order to effectively conduct the supervision of inventory counting, CPA should make agreement with audit client on relevant issues, but CPA should avoid audit client knowing the inventory items that are being subject to audit tests.

【答案解析】

【答疑编号10585836】

<4>、

【正确答案】不妥当。

理由:在检查时,注册会计师应当从存货盘点记录中选取项目追查至存货实物,以测试盘点记录的准确性;注册会计师还应当从存货实物中选取项目追查至存货盘点记录,以测试存货盘点记录的完整性。

Inappropriate.

Reason: During inspection, CPA should select a sample from inventory count sheet and vouch it to physical asset, to ensure the accuracy of the inventory records; CPA should also select a sample from physical asset and trace it to inventory count sheet to ensure the completeness of the inventory records.

【答案解析】

【答疑编号10585837】

<5>、

【正确答案】不妥当。

理由:对于正在加工中的存货实施程序存在不当之处。应当获取盘点日前后存货收发及移动的凭证,检查库存记录与会计记录期末截止的正确性。

Inappropriate.

Reason: It is inappropriate for the audit procedures carried out on those inventories manufactured in progress. The source documents for the movement of inventories before and after the counting date should be obtained, checking the accuracy of the cut-off between warehouse records and accounting records.

【答案解析】

【答疑编号10585838】

<6>、

【正确答案】不妥当。

理由:对于盘盈或盘亏的存货,不应由仓库保管人员对于存货实物数量和仓库存货记录进行调节。应由乙公司组成调查小组对盘盈或盘亏进行分析和处理(复核确认),并将存货实物数量和仓库记录调节相符。

Inappropriate.

Reason: For those inventory surplus or inventory shortages, the quantities of physical assets and the warehouse inventory records should not be adjusted by warehouse keeper.

【答案解析】

【答疑编号10585839】

<7>、

【正确答案】不妥当。

理由:因为本题的盘点日不是资产负债表日,注册会计师还应当实施适当的审计程序,确定盘点日与资产负债表日之间存货的变动是否已作正确的记录。

Inappropriate.

Reason: Because the counting date is not the balance sheet date in this case, CPA should also perform appropriate audit procedures to determine whether correct records are made as to the movements between counting date and the balance sheet date.

【答案解析】本题考核“存货监盘(非特殊类型存货监盘)”这个知识点。

5.

ABC会计师事务所的A注册会计师作为审计项目合伙人负责审计甲公司2012年度财务报表。审计项目组针对甲公司应收账款实施函证程序时,决定采用PPS抽样方法实施抽样。甲公司应收账款包含2000笔明细账户,账面总金额为1000万元。A注册会计师确定的可接受误受风险为5%。其他相关事项如下:

(1)在确定样本规模后,A注册会计师认为,PPS抽样方法的抽样单元是货币单元,而实施审计测试需要针对应收账款明细账户的实物单元。为了在选取样本时找到与被选中的特定货币单元相关联的明细账户的实物单元,A注册会计师逐项累计总体中所有项目的账面金额。

(2)假设经过计算,样本规模是200,A注册会计师利用系统选样方法选取了200个样本。(3)A注册会计师对这200个样本对应的应收账款明细账注明的甲公司的债权人分别发出积极式询证函,其中有三个债权人的回函始终没有收到,A注册会计师认为不存在错报,没有实施进一步审计程序。

(4)假设A注册会计师对选出的200个样本项目分别发出积极式询证函都收到了回函,在进行测试后发现两个错报,一个是账面金额为1000元的明细账户中存在500的高估错报;另一个是账面金额为2000元的明细账户中有1400元的高估错报。A注册会计师利用样本错报的相关信息计算总体错报上限。在误受风险为5%的情况下,高估错报为0、1、2时的PPS抽样风险系数分别为:3.00、4.75、6.30。

要求:

<1> 、简要说明A注册会计师利用PPS抽样方法在确定样本规模时需要考虑的因素。

<2> 、针对上述(1)至(3)项,分别指出A注册会计师的做法是否存在不当之处。如果存在不当之处,请简要说明理由。

<3> 、单独考虑事项(4),代A注册会计师计算总体错报上限。

<4> 、如果应收账款认定层次的实际重要性水平是20万元,请分析甲公司应收账款是否存在重大错报,如果存在重大错报,A注册会计师应实施什么应对措施?

<1>、

【正确答案】结合PPS抽样样本规模公式可知,PPS抽样确定样本规模必须考虑的因素包括:总体账面价值、风险系数、可容忍错报、预计总体错报、扩张系数。

Combined with PPS sample size formula, when determining the sample size in PPS sampling, the factors that must be considered include the carrying value of population, risk coefficient, tolerable misstatement, expected misstatement on population, expansion factor.

【答案解析】

【答疑编号10586106】

<2>、

【正确答案】事项(1)正确。

事项(2)正确。

事项(3)不正确。注册会计师应当考虑与被询证者联系,要求对方作出回应或再次发函,如果仍未得到被询证者回复,应该实施替代审计程序。

Event (1) is correct.

Event (2) is correct.

Event (3) is incorrect. CPA should consider to contact with the persons who accept the confirmation, require them to response or send the second confirmation, if no response, alternative audit procedures should be performed.

【答案解析】

【答疑编号10586107】

<3>、

【正确答案】总体错报上限=基本界限+第一个错报所增加的错报上限+第二个错报所增加的错报上限

基本界限=1000×3.0/200×1=15(万元)

t1=1400/2000=0.7

t2=500/1000=0.5

第一个错报所增加的错报上限=1000×(4.75-3.0)/200×0.7=6.125(万元)

第二个错报所增加的错报上限=1000×(6.30-4.75)/200×0.5=3.875(万元)

总体错报上限=15+6.125+3.875=25(万元)

Upper limit for the misstatement on population+upper limit increased for the 1st misstatement+ Upper limit increased for the 2nd misstatement

Basic limit=1000×3.0/200×1=15(ten thousand yuan)

t1=1400/2000=0.7

t2=500/1000=0.5

Upper limit increased for the 1st misstatement=1000×(4.75-3.0)/200×0.7=6.125(ten thousand yuan)

Upper limit increased for the 2nd misstatement=1000×(6.30-4.75)/200×0.5=3.875(ten thousand yuan)

Upper limit for the misstatement on population=15+6.125+3.875=25(ten thousand yuan)

【答案解析】

【答疑编号10586108】

<4>、

【正确答案】由于计算的总体错报上限25万元超过了应收账款认定层次的可容忍错报20万元,表明应收账款存在重大错报,注册会计师不能接受应收账款账面金额,应扩大样本规模进一步检查。

Since upper limit for the misstatement on population of 250,000 yuan which exceeds tolerable misstatement of 200,000 yuan that is related to account receivable account on assertion level, it indicates that there are material misstatement in account receivable, CPA should not accept carrying value of account receivable, and should make further inspection by enlarging the sample size.

【答案解析】本题考核“审计抽样(PPS抽样)”这个知识点。

【答疑编号10586109】

6.

ABC会计师事务所通过招投标程序接受委托,负责审计上市公司甲公司(工业企业)2013年度财务报表,并委派A注册会计师为项目合伙人,在招投标阶段和审计过程中,ABC会计师事务所遇到下列与职业道德有关的事项:

(1)甲公司2013年1月1日为审计项目合伙人A注册会计师的女儿开设的X公司提供贷款,贷款额度为500万元,期限为一年。

(2)签订审计业务约定书时,ABC会计师事务所根据有关部门的要求,与甲公司商定按六折收取审计费用,据此,审计项目组计划相应缩小审计范围,并就此事与甲公司治理层达成一致意见。

(3)签订审计业务约定书后,ABC会计师事务所发现甲公司与本事务所另一常年审计客户乙公司存在直接竞争关系。ABC会计师事务所未将这一情况告知甲公司和乙公司。

(4)Z公司为甲公司的合营企业,2013年2月2日事务所合伙人B注册会计师的儿子小李购买了Z公司50%的股权。

(5)审计过程中,适逢甲公司招聘高级管理人员,A注册会计师应甲公司的要求对可能录用人员的证明文件进行检查,并就是否录用形成书面意见。

(6)ABC会计师事务所合伙人C不属于审计项目组成员,其妻子继承父亲遗产,其中包括甲公司内部职工股份10000股。

要求:

<1>、针对上述(1)至(6)项,分别指出ABC会计师事务所是否违反中国注册会计师职业道德守则,并简要说明理由。

<1>、

【正确答案】(1)违反。甲公司作为非银行或类似金融机构的审计客户为审计项目合伙人的主要近亲属(A注册会计师的女儿)提供巨额贷款,因自身利益产生对独立性的不利影响,导致没有防范措施能够将其降低至可接受的水平。

(2)违反。虽然说事务所可以自主商定审计的收费,但是不能因为收费而相应缩小审计范围,影响审计工作的质量。

(3)违反。事务所如同时为两个存在竞争关系的审计客户提供审计,需要告知客户,并征得他们的同意才能执行业务。

(4)违反。事务所合伙人B注册会计师的主要近亲属(其儿子)与甲公司共同在Z公司中拥有直接经济利益,因自身利益产生对独立性的不利影响。

(5)违反。根据规定对属于公众利益实体的审计客户而言,招聘董事、高级管理人员,或所处职位能够对客户会计记录或被审计财务报表的编制实施重大影响的人员,会计师事务所不能提供对可能录用的候选人的证明文件进行核查的服务。

(6)违反。如果会计师事务所的合伙人的主要近亲属通过继承等方式从甲公司获得直接经济利益,将会因自身利益产生对独立性的不利影响。

[Answer]

(1) It is in violation of the law. Company Jia is a audit client which is not a bank or similar financial institution, it issues huge debts to audit partner’s immediate relative (CPA A’s daughter), it will lead to adverse impact on independence due to self interest, and no safeguards to prevent it to acceptable level.

(2) It is in violation of the law. Although accounting firm could actively negotiate audit fees, the scope of audit should not be narrowed due to the fees charged, otherwise it will affect

the quality of the audit work.

(3) It is in violation of the law. Accounting firm provide services to two clients who are competing with each other, it should notify both clients and can only carry out its engagement with clients consent.

(4) It is in violation of the law. The immediate relative (his son) of the audit partner, CPA B has direct financial interest in Company Z, together with Company Jia, it will have adverse impact on the independence due to self interest.

(5) It is in violation of the law. In accordance with the law, for those audit clients who are public interest entities, if board of directors, senior management or other personnel who have significant influence on client’s accounting records or preparation of financial statements that subject to audit have been hired, accounting firm could not provide services in relation to verification of potential candidates’ documents.

(6) It is in violation of the law. If audit partner’s immediate relatives obtaine direct financial benefits from Company Jia through inheritance mode, it will have adverse impact on independence as a result of self interest.

7.

6、A 注册会计师是甲公司2012 年度财务报表审计业务的项目合伙人。根据评估的重大错报风险,A 注册会计师决定针对应收账款项目的计价和分摊目标实施传统变量抽样,以确定

财务报表上列示的应收账款是否存在高估或低估。A 注册会计师确定的应收账款项目的可容

忍误差为21000 元。由于预计只存在少量差异,确定的预计总体错汇报为0。其他相关情况如下:

(1)A 注册会计师将甲公司2012 年12 月31 日应收账款明细表中列示的全部应收账款定

义为抽样总体,而将明细表中涉及的每个客户定义为抽样单元。

(2)在确定样本规模时,为在确保审计效果的前提下提高审计的效率,同时考虑到风险后果的严重性,A 注册会计师确定的误受风险为5%,误拒风险为10%。

(3)为实现计价和分摊目标,A 注册会计师计划对抽取的抽样单元实施积极方式的函证程序,并针对无法收到回函等特殊情况计划了替代审计程序。

(4)对样本实施审计程序后,确认的样本审定金额与样本的账面金额非常接近。A 注册会计师据此认为在推断总体错报点估计值时采用差额估计抽样和比率估计抽样更为适宜。(5)A 注册会计师为计算总体错报上限,认为应根据总体规模、样本规模、样本标准差和可接受的误拒风险系数计算抽样风险允许限度。

要求:单独考虑上述每一种情况,请指出A 注册会计师的决策和做法是否恰当。如果认为不恰当,请简要说明理由。

【正确答案】:(1)不恰当。与计价和分摊目标相关的审计程序是针对单笔应收账款实施的,

应将明细表中列示的每一笔应收账款定义为抽样单元。

(2)恰当。

(误受风险影响审计效果,误拒风险影响审计效率,因此误受风险的后果更为严重,故可接受的误受风险水平应低于误拒风险水平。)

(3)不恰当。仅实施函证程序无法证实应收账款的计价和分摊认定。A 注册会计师应同时实施分析应收账款账龄、检查坏账准备计提等必要审计程序。

(4)不恰当。使用统计抽样时,如果预计只发现少量差异,不应使用比率估计抽样和差额估计抽样。

(5)不恰当。在计算抽样风险允许限度时,需要利用可接受的误受风险系数,与可接受的误拒风险系数不相关。

Answer:

(1) is inappropriate. The audit procedures related to the target of valuation and allocation

is performed for every single account receivable transaction; it is required to define every

single account receivable transaction as sampling unit on the transaction lists.

(2) is appropriate. The acceptance risk has adverse impact on the effectiveness of audit; rejection risk has adverse impact on the efficiency of audit. Therefore, the outcome of acceptance risk is more serious, thus the acceptable level of rejection risk should be lower

than that of the level of acceptance risk.

(3) inappropriate. The valuation and allocation of account receivable cannot be confirmed

if only carrying out confirmation procedures. A CPA should carry out the analysis of accounts receivable check bad debt provisions, and other necessary audit procedures at the same time

(4) inappropriate. If only small differences are found in audit sampling, then the ratio estimation sampling and difference estimation sampling should not be used.

(5) inappropriate. The coefficient of acceptable acceptance risk should be used in the calculation of the limits of sampling risk, which is not related to the coefficient of acceptable rejection risk.

Date: 2013.7.20

8.

、ABC会计师事务所负责审计上市公司甲公司2011年度财务报表,并委派A 注册会计师担任审计项目合伙人。在审计过程中,审计项目组遇到下列与职业道德有关的事项:(1)甲公司已连续两年积欠审计费用,至今尚未偿还,甲公司承诺审计后付清,ABC会计师事务所决定继续承接本年甲公司的审计业务。

(2)A 注册会计师在审计中还发现,ABC会计师事务所的合伙人X 的妻子是甲公司的高管,

持有该公司5%的股票期权。但合伙人X 不是该项目的合伙人。

10 2013 面授学员内部专享

(3)由于A 注册会计师在执行业务过程中表现出高超的专业素质,甲公司聘请A 注册会计

师作为税务纠纷的辩护人。A 注册会计师接受这项工作。

(4)审计过程中,适逢甲公司招聘高级管理人员,A 注册会计师应甲公司的要求对可能录用人员的证明文件进行检查,并就是否录用形成书面意见。

(5)ABC会计师事务所的办公用房系从甲公司优惠租用的。

(6)A 注册会计师在审计中发现,甲公司与ABC会计师事务所都向同一银行借款,数额比

较巨大,ABC会计师事务所享受了贷款利率优惠。

要求:

针对上述(1)至(6)项,逐项指出ABC会计师事务所及其人员是否违反中国注册会计师职业道德守则,并简要说明理由。

【正确答案】:(1)违反。如果客户长期未支付应付的审计费,会因自身利益产生不利影响。

(2)违反。项目合伙人所在分部的其他合伙人或主要近亲属在审计客户中拥有直接经济利益会影响独立性。

(3)违反。在审计客户与第三方发生诉讼或纠纷时,注册会计师担任该客户的辩护人,将产生过度推介对独立性的不利影响。

(4)违反。注册会计师为被审计单位提供高级管理人员招聘服务,可能因自身利益、密切关系或外在压力对独立性产生不利影响。

(5)违反。优惠租用办公用房会产生经济利益的不利影响。

(6)不违反。双方不存在直接的经济利益关联。

[Answer]

(1) Rules are violated. If customers have not paid audit fees payable for a long period, detrimental effects will arise from their own interests.

(2) Rules are violated. If other partners in the division or close relatives of the project

partner have direct economic interests in the audit client, the independence will be

affected.

(3) Rules are violated. If the CPA acts as the audit client's advocate in event of litigation or disputes with third parties, the independence will be detrimentally affected due to

excessive referrals.

(4) Rules are violated. When the CPA provides senior management recruitment services

for the auditee, the independence may be detrimentally affected due to his own interests,

their close relationship or external pressure.

(5) Rules are violated. The preferential renting of the office premises will have detrimental effects due to economic interests.

(6) Rules are not violated. Both parties do not have economic interests directly associated with each other.

9.

、ABC 会计师事务所接受X 股份有限责任公司(以下简称X 公司)董事会委托,对公司2011 年度财务报表进行审计。X 公司采用手工会计系统。工作底稿中记载的有关X 公司内

部控制设计和运行的部分内容摘录如下:

(1)为加强货币支付管理,货币资金支付审批实行分级管理办法;单笔付款金额在10 万2013 面授学员内部专享10

Date: 2013.9.6 内部资料

元以下的,由财务部经理审批;单笔付款金额在10万元以上、50万元以下的,由财务总监审核;单笔付款金额在50万元以上的,由总经理审批。

(2)在发出原材料过程中,仓库部门根据生产部门开出的领料单发出原材料。领料单必须列明所需原材料的数量和种类,以及领料部门的名称。领料单可以一料一单,也可以多料一单,通常需一式两联,仓库部门发出原材料后,其中一联连同原材料交还领料部门,一联留仓库部门据以登记原材料明细账。

(3)为加强在建工程项目的管理,要求审批人根据工程项目相关业务授权批准制度的规定,在授权范围内进行审批,不得超过审批权限。经办人在职责范围内,按照审批人的批准意见办理工程项目业务。对于审批人超越授权范围审批的工程项目业务,经办人应在办理后,及时向审批人的上级授权部门报告。

(4)丙职员在核对商品装运凭证和相应的经批准的销售单后,开具销售发票。具体程序为:根据已授权批准的商品价目表填写销售发票的金额,根据商品装运凭证上的数量填写销售发票的数量;销售发票的其中一联交财务部丁职员据以登记与销售业务相关的总账和明细账。要求:假定X 公司的其他内部控制不存在缺陷,请指出X 公司内部控制在设计与运行方面

的缺陷,并简要说明理由。

【正确答案】:(1)存在缺陷。“单笔付款金额在50万元以上的,由总经理审批”不恰当。公

司对于重要货币资金支付业务,应当实行集体决策和审批。因此,对公司总经理的货币资金支付审批权限,也应设定上限,超过设定审批权限的,应由公司集体决策和审批。

(2)存在缺陷。财务部无领料单不恰当。财务部在原材料收发核算时应获得、审核领料单。(3)存在缺陷。允许经办人在明知越权审批的情况下仍然先办理后报告,不恰当。这种设计将使得关键内部控制失去意义。

(4)存在缺陷。丁职员一人登记与销售业务相关的总账和明细账,不恰当。与销售业务相关的总账和明细账的登记属于不相容职务,应当予以分离。

(1)has defects. The statement that “single transaction exceeds 500000 Yuan is

required to be approved by general manager”is inappropriate. Company should

Date: 2013.9.6 内部资料

implement group discussion and approval for important monetary payments. Therefore, it is required to set a corresponding approval limit on the general manager, and the exceeding amount should be determined collectively.

(2)has defects. It is inappropriate that financial department does not have requisitions. Financial department is supposed to obtain and check requisitions at the time of receiving and delivery of raw materials.

(3)has defects. Having known that making the approval is beyond the authority, the responsible person still handled the issue before reported it, which was inappropriate. This design would make the key internal control lost its meaning.

(4)has defects. It is inappropriate for D staff both records the general ledger and subsidiary ledger related to sales. The record of general ledger and subsidiary ledger related to sales are two incompatible duties which should be separated.

10.

、2011 年12 月10 日,ABC 会计师事务所与乙公司签订了该公司2011 年度财务报表审计业务约定书,并任命A 和 B 注册会计师为项目经理。按照业务约定,ABC会计师事务所

应在2011 年12月18日开始审计工作。A 和B注册会计师确定的乙公司年度财务报表层次

的重要性水平为15万元。

经过了解,得知乙公司是一家生产和销售酒产品的公司,其产品主要向某些大型客户直销。直销的产品根据客户订单和需求量预测报告生产,并在产品包装上印有客户名称和标志;除此之外,乙公司还向部分省、市级经销商销售,并根据经销商的订单生产。

资料一:

存货是A 和B 注册会计师对乙公司确定的重点审计领域。按照ABC会计师事务所与乙公司

的约定,A和B 注册会计师于2011 年12月25日对存货实施监盘程序。Date: 2013.8.7 内部资料

在对存货进行盘点前,A 和 B 注册会计师于12 月24 日对乙公司的仓库进行了观察,并在

拟检查的存货项目上作出标识。存放在乙公司的成品仓储区的存货主要包括:

(1)已装箱、打包完毕,并贴上运输单的各种酒类制品5000 箱。运输单盖承运商的业务章,填有商品名称、规格、数量、承运商名称、发货日期、运输目的地、经销商名称与电话号码等;

(2)在包装物上印有终端客户名称和标志的各种特制酒类制品共计3000 箱;

(3)已灌装完毕但尚未贴上标签纸(根据订单在包装瓶上贴不同的标签纸)的各种酒制品12000 木箱(特制大木箱,由叉车直接从生产流水线运到仓库)。木箱外标有商品名称、型号、数量、生产班组负责人签名;

存放在乙公司原材料仓库的存货包括:

(4)各种制酒用原材料30种,存放在直径10米,高20米的50个木桶中;

(5)各种品种的液体原材料10 种,存放在直径40 厘米、高40 厘米的8000 个密封铝桶

中,外包装上印有供应商名称、品名、数量、价格;

资料二:

2012 年2 月27 日,注册会计师对乙公司截至当日的期后事项进行了审计,获悉作为乙公司直销终端客户向人民法院提起诉讼,要求乙公司赔偿其100 万元。起诉的主要原因是该客户饮用乙公司的酒产品,导致其身体产生多种不良反应。经向律师了解,乙公司在酒制品中加入过量甲醇导致,该诉讼很可能支付赔偿款20万元。A 和 B 注册会计师要求乙公司据

此计提预计负债20万元。

要求:

(1)针对资料一,回答下列问题:

①请指出在监盘之前对成品仓库进行现场观察时,注册会计师应重点核实的内容,并简要列示相应的审计程序,并同时指出在对存货进行盘点前的相关工作是否恰当;

②假定注册会计师对乙公司原材料的盘点程序不满意,请指出注册会计师及审计小组的专家

(完整版)审计常用英文词汇

审计常用英文词汇 1.Assurance engagements and external audit 鉴证业务和外部审计 Materiality,true and fair presentation,reasonable assurance 重要性,真实、公允反映,合理保证 Appointment,removal and resignation of auditors 注册会计师的聘用,解聘和辞职 Types of opinion:unmodified opinion,modified opinion,adverse opinion,disclaimer of opinion 审计意见类型:无保留意见,保留意见,否定意见,无法表示意见 Professional ethics:independence,objectivity,integrity,professional competence,due care,confidentiality, professional behavior 职业道德:独立、客观和公正,专业胜任能力,应有的关注,保密性,职业行为 Engagement letter 审计业务约定书 2.Planning and risk assessment 审计计划和风险评估 General principles 一般原则 Plan and perform audits with an attitude of professional skepticism 计划和执行审计业务应保持应有的职业怀疑态度 Audit risks = inherent risk ×control risk ×detection risk 审计风险=固有风险×控制风险×检查风险 Risk-based approach 风险导向型审计 Understanding the entity and knowledge of the business 了解被审单位 Assessing the risks of material misstatement and fraud 估计重大错报或舞弊的风险 Materiality (level),tolerable error 重要性水平,可容忍误差 Analytical procedures 分析性复核程序 Planning an audit 制定审计计划 Audit documentation:working papers 审计记录:工作底稿 The work of others 利用其他人的工作 Rely on the work of experts 利用专家工作 Rely on the work of internal audit

会计审计英语词汇大全

1 ability to perform the work能力履行工作 2 acceptance procedures承兑程序过程 3 accountability经管责任,问责性 4 accounting estimate会计估计 5 accounts receivable listing应收帐款挂牌 6 accounts receivable应收账款 7 accruals listing应计项目挂牌 8 accruals应计项目 9 accuracy准确性 10 adverse opinion否定意见 11 aged analysis年老的分析(法,学)研究 12 agents代理人 13 agreed-upon procedures约定审查业务 14 analysis of errors错误的分析(法,学)研究 15 anomalous error反常的错误 16 appointment ethics任命伦理学 17 appointment任命 18 associated firms联合的坚挺 19 association of chartered certified accounts(ACCA)特计的证(经执业的结社(ACCA) 20 assurance engagement保证债务

21 assurance保证 22 audit审计,审核,核数 23 audit acceptance审计承兑 24 audit approach审计靠近 25 audit committee审计委员会,审计小组 26 ahudit engagement审计业务约定书 27 audit evaluation审计评价 28 audit evidence审计证据 29 audit plan审计计划 30 audit program审计程序 31 audit report as a means of communication审计报告如一个通讯方法32 audit report审计报告 33 audit risk审计风险 34 audit sampling审计抽样 35 audit staffing审计工作人员 36 audit timing审计定时 37 audit trail审计线索 38 auditing standards审计准则 39 auditors duty of care审计(查帐)员的抚养责任 40 auditors report审计报告 41 authority attached to ISAs代理权附上到国际砂糖协定

会计方面专业术语的英文翻译

会计方面专业术语的xx acceptance承兑 account账户 accountant会计员 accounting会计 accounting system会计制度 accounts payable应付账款 accounts receivable应收账款 accumulated profits累积利益 adjusting entry调整记录 adjustment调整 administration expense管理费用 advances预付 advertising expense广告费 agency代理 agent代理人 agreementxx allotments分配数 allowance津贴 amalgamation合并 amortization摊销

amortized cost应摊成本 annuities年金 applied cost已分配成本 applied expense已分配费用 applied manufacturing expense己分配制造费用apportioned charge摊派费用 appreciation涨价 article of association公司章程 assessment课税 assets资产 attorney fee律师费 audit审计 auditor审计员 average平均数 average cost平均成本 bad debt坏账 balance余额 balance sheet资产负债表 bank account银行账户 bank balance银行结存 bank charge银行手续费

bank deposit银行存款 bank discount银行贴现bank draft银行汇票 bank loan银行借款 bank overdraft银行透支bankers acceptance银行承兑bankruptcy破产 bearer持票人 beneficiary受益人 bequest遗产 bill票据 bill of exchange汇票 bill of lading提单 bills discounted贴现票据bills payable应付票据 bills receivable应收票据board of directors董事会bonds债券 bonus红利 book value账面价值bookkeeper簿记员

审计报告中的会计及审计英语 (2)

年度审计报告中的会计及审计英语 English for Accounting & Auditing in Annual Repor 主要内容 Contents 年度审计报告框架 Framework of Annual Report 年度审计报告中所应用的相关专业会计及审计英语 Accounting and Audit English in Annual Report 年度审计报告框架 Framework of Annual Report 审计意见Audit opinion 管理层责任Management’s Responsibility for the Financial Statements 注册会计师责任Auditors’ Responsibility 审计意见Auditor’s Opinion 管理层财务报表Management Financial statements 资产负债表Balance Sheet 利润表Income Statements 现金流量表Cash flow statement 财务报表附注Notes to the financial statements 年度审计报告范例-管理层责任(1) Example - Management’s Responsibility(1) 按照中华人民共和国财政部颁布的企业会计准则的规定编制财务报表是贵公司管理层的责任。 The Company’s management is responsible for the pre paration of these financial statements in accordance with China Accounting Standards for Business Enterprises issued by the Ministry of Finance of the People’s Republic of China. 年度审计报告范例-管理层责任(2) Example - Management’s Responsibility (2) 这种责任包括:(1)设计、实施和维护与财务报表编制相关的内部控制,以使财务报表不存在由于舞弊或错误而导致的重大错报;(2)选择和运用恰当的会计政策;(3)作出合理的会计估计。 This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation of financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

审计考试英语

1.accounting is the system that measures business activities, processes that information into reports, and communicates the results to decision-makers. 会计是计量企业经济活动,处理并加工经济信息,并将处理结果与决策者进行交流的信息系统。 2.managers of businesses and other users use accounting information to set goals for their organizations, to evaluate progress toward those goals, and to take corrective action if necessary. 企业管理者及其他会计信息使用者利用会计信息为企业和团体制定目标,评价为实现目标而付出的努力,并在必要时采取改进措施。 3、accounting may be divided into two parts:financial accounting and management accounting. 会计可以分为财务会计与管理会计两部分。 4、management accounting, or managerial accounting, provides information mainly to management of a firm, analyzing individual and specific problems for decision making in various departments of a business. 管理会计主要对企业的管理层提供信息,作为企业内部各个部门进行决策的依据。 5、in contrast, financial accounting is related to preparation of reports and statements for users both inside and outside a firm.

常用审计英语词汇

常用审计英语词汇 1 ability to perform the work 能力履行工作 2 acceptance procedures 接受程序 3 accountability 经管责任,问责性 4 accounting estimate 会计估计 5 accounts receivable listing 应收账款列表 6 accounts receivable 应收账款 7 accruals listing 应计项目列表 8 accruals 应计项目 9 accuracy 准确性 10 adverse opinion 否定意见 11 aged analysis 账龄分析 12 agents 代理人 13 agreed-upon procedures 约定审查业务 14 analysis of errors 错误分析 15 anomalous error 反常的错误 16 appointment ethics 接受任命的相关职业道德考虑 17 appointment 任命 18 associated firms 关联公司 19 association of chartered certified accounts(ACCA)英国特许注册会计师公会 20 assurance engagement 保证约定

21 assurance 保证 22 audit 审计,审核,核数 23 audit acceptance 接受审计 24 audit approach 审计方法 25 audit committee 审计委员会,审计小组 26 audit engagement 审计业务约定书 27 audit evaluation 审计评价 28 audit evidence 审计证据 29 audit plan 审计计划 30 audit program 审计程序 31 audit report as a means of communication 作为沟通方式的审计报告 32 audit report 审计报告 33 audit risk 审计风险 34 audit sampling 审计抽样 35 audit staffing 审计工作人员调配 36 audit timing 审计时间安排 37 audit trail 审计线索 38 auditing standards 审计准则 39 auditors duty of care 审计人员的审慎职责 40 auditors report 审计报告 41 authority attached to ISAs 遵守国际审计准则

审计英语词汇

审计英语词汇 audit 审计 attestation 鉴证 audit of financial statements 财务报表审计 high levels of assurance 高水平保证 compilation 编制 reliability 可靠性 relevance 相关性 professional skepticism 职业谨慎 objectivity 客观性 professional competence 专业胜任能力 audit engagement letter 业务约定书 the client 委托人 the existing CPA 现任注册会计师 the successor CPA 后任注册会计师 the preceding CPA前任注册会计师 issue the audit report 出具审计报告 the board of directors 董事会 determine the nature, timing and extent of the audit procedures 确定审计程序的性质、时间和范围 a general knowledge of ——初步了解―――的情况 a more knowledge of——进一步了解的情况 the prior year’s working papers 以前年度工作底稿 minutes of meeting 会议纪要 business risks 经营风险 accounting estimate 会计估计 management representations 管理层声明

going concern assumption 持续经营假设 audit plan 审计计划 fraud舞弊 misappropriation of assets 侵占资产 materiality 重要性 misstatements or omissions 错报或漏报 subsequent events 期后事项 audit risk 审计风险 detection risk 检查风险 inappropriate audit opinion 不适当的审计意见 material misstatement 重大的错报 tolerable misstatement 可容忍错报 the acceptable level of detection risk 可接受的检查风险walk-through test 穿行测试 flow chart 流程图 audit evidence 审计证据 substantive procedures 实质性程序 assertions 认定 existence 存在 occurrence 发生 completeness 完整性 rights and obligations 权利和义务 valuation and allocation 计价和分摊 cutoff 截止 accuracy 准确性 classification 分类 inspection 检查 supervision of counting 监盘

审计英文词汇整理

1.audit 审计 2.attestation 鉴证 3.credibility 可信赖程度 4.audit of financial statements 财务报表审计 5.agreed-upon procedures 执行商定程序 6.high levels of assurance 高水平保证 https://www.wendangku.net/doc/7a14380054.html,pilation 编制 8.reliability 可靠性 9.relevance 相关性 10.professional skepticism 职业谨慎 11.objectivity 客观性 12. professional competence 专业胜任能力 13.Senior/CPA-in-charge 项目经理 14.audit engagement letter 业务约定书 15.recurring audit 连续审计 16.the client 委托人 17.change CPA更换注册会计师 18.the existing CPA 现任注册会计师 19.the successor CPA 后任注册会计师 20.the preceding CPA前任注册会计师 21.issue the audit report 出具审计报告 22.expert 专家 23.the board of directors 董事会 24.knowledge of the entity‘ s business 了解被审计单位情况 25.assess material misstatement risks评估重大错报风险 26.detemine the nature,timing and extent of the audit procedures 确定审计程序的性质、时间和范围 27.a general knowledge of 初步了解―――的情况 28.a more knowledge of 进一步了解的情况 29.the prior year‘s working papers 以前年度工作底稿 30.minutes of meeting 会议纪要 31.business risks 经营风险 32.appropriateness适当性 33.accounting estimate 会计估计 34.management representations 管理层声明 35.going concern assumption 持续经营假设 36.audit plan 审计计划 37.significant audit areas 重点审计领域 38.error 错误 39.fraud舞弊 40.modified or additional procedures 修改或追加审计程序 41.misappropriation of assets 侵占资产42.transactions without substance 虚假交易 43.unusual pressures 异常压力 44.the suspected noncompliance 涉嫌存在违法行为 45.materialiy 重要性 46.exceed the materiality level 超过重要性水平 47.approach the materiality level 接近重要性水平 48.an acceptably low level 可接受水平 49.the overall financial statement level and in related account balances and transaction levels 财务报表层和相关账户、交易层 50.misstatements or omissions 错报或漏报 51.aggregate 总计 52.subsequent events 期后事项 53.adjust the financial statements 调整财务报表 54.perform additional audit procedures 实施追加的审计程序 55.audit risk 审计风险 56.detection risk 检查风险 57.inappropriate audit opinion 不适当的审计意见 58.material misstatement 重大的错报 59.tolerable misstatement 可容忍错报 60.the acceptable level of detection risk 可接受的检查风险 61.assessed level of material misstatement risk 重大错报风险的评估水平 62.simall business 小规模企业 63.accounting system 会计系统 64.test of control 控制测试 65.walk-through test 穿行测试 https://www.wendangku.net/doc/7a14380054.html,munication沟通 67.flowchart 流程图 68.reperformance of internal control 重新执行 69.audit evidence 审计证据 70.substantive procedures 实质性程序 71.assertions认定 72.esistence存在 73.occurrence发生 https://www.wendangku.net/doc/7a14380054.html,pleteness完整性 75.rightsand obligations 权利和义务 76.valuationand allocation 计价和分摊 77.cutoff截止 78.accuracy准确性 79.classification分类 80.inspection检查 81.supervision of counting 监盘 82.observation观察

常用审计英语术语

accounting estimate 会计估计 accounts receivable 应收账款 accruals listing 应计项目挂牌 accruals 应计项目 accuracy 准确性 adverse opinion 否定意见 agreed-upon procedures 约定审查业务 analysis of errors 错误的分析(法,学)研究anomalous error 反常的错误 association of chartered certified accounts(ACCA)assurance engagement 保证约定 assurance 保证 audit 审计,审核,核数 audit acceptance 审计承兑 audit approach 审计靠近 audit committee 审计委员会,审计小组 audit engagement 审计业务约定书 audit evaluation 审计评价 audit evidence 审计证据 audit plan 审计计划 audit program 审计程序 audit report 审计报告 audit risk 审计风险 audit sampling 审计抽样 audit staffing 审计工作人员 audit timing 审计定时 audit trail 审计线索 auditing standards 审计准则 auditors report 审计报告 bad debts 坏账 bank 银行 bank reconciliation 银行对账单,余额调节表beneficial interests 受益权 business risk 经营风险 cash count 现金盘点 confidence 信任 confidentiality 保密性 confirmation of accounts receivable 应收账款的查证conflict of interest 利益冲突 contingent asset 或有资产 contingent liability 或有负债 control environment 控制环境 control procedures 控制程序 control risk 控制风险

审计报告模板英文

英文审计报告模板 审计报告 2009-05-20 21:52:50 阅读260 评论0 字号:大中小订阅 审计报告 auditors’ report 安永华明(2007)审字第 xxxxx 号 ernst & young hua ming (2007) audit no. xxxxxxxx abc股份有限公司全体股东: 我们审计了后附的abc股份有限公司(以下简称“贵公司”)及其子公司和合营企业(以下 统称“贵集团”)财务报表,包括2006年12月31日的合并及母公司资产负债表、2006年度 的合并及母公 司利润及利润分配表、股东权益增减变动表和现金流量表以及财务报表附注。 accounting policies and other explanatory notes. 一、管理层对财务报表的责任 按照企业会计准则和《企业会计制度》的规定编制财务报表是贵公司管理层的责任。这 种责任包括:(1) 设计、实施和维护与财务报表编制相关的内部控制,以使财务报表不存在 由于舞弊或错 误而导致的重大错报;(2) 选择和运用恰当的会计政策;(3) 作出合理的会计估计。 1. management’s responsibility for the financial statements the management is responsible for the preparation and fair presentation of these financial statements in accordance with the accounting standards for business enterprises and china accounting system for business enterprises. this responsibility includes: (i) designing, implementing and maintaining (转载于:审计报告模板英文)internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error; (ii) selecting and applying appropriate accounting policies; and (iii) making accounting estimates that are reasonable in the circumstances. 二、注册会计师的责任 我们的责任是在实施审计工作的基础上对财务报表发表审计意见。我们按照中国注册会 计师审计准则的规定执行了审计工作。中国注册会计师审计准则要求我们遵守职业道德规范, 计划和实施 审计工作以对财务报表是否不存在重大错报获取合理保证。 2. auditor’s responsibility from material misstatement. 审计工作涉及实施审计程序,以获取有关财务报表金额和披露的审计证据。选择的审计 程序取决于注册会计师的判断,包括对由于舞弊或错误导致的财务报表重大错报风险的评估。 在进行风险评估时,我们考虑与财务报表编制相关的内部控制,以设计恰当的审计程序,但 目的并非对内部控制的有效性发表意见。审计工作还包括评价管理层选用会计政策的恰当性 和作出会计估计的合 理性,以及评价财务报表的总体列报。 an audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. the procedures selected depend on the auditor’s judgment, including the assessment of the risks of material

注册会计师审计英语词汇整理

财会英语词汇(审计)(1) 1.appointment, removal and resignation of auditor 注册会计师的任命、解聘和辞职 2.fundamental principles 基本原则 3.professional ethics 职业道德 4.integrity [?n'tegr?t?] n. 诚信 5. objectivity/subjectivity 客观性/主观性 6.professional competence and due care专业胜任 能力和应有的关注 7. confidentiality [?k?nfi?den?i'?liti] n.保密 8.independence [?nd?'pend(?)ns] n. 独立,独立性 9. bias ['ba??s] n. 偏见 10.safeguard['se?fgɑ:d] n. 防范措施 11.engagement [?n'ge?d?m(?)nt;en-] n. 约会,诺言,婚约;在审计中意为“与客户签订的业务约定”。 12. self-interest n. 自身利益 13.employment with assurance client 与审计客户 发生雇佣关系 14.gifts and hospitality 礼品和款待 15.advocacy['?dv?k?s?] n. 过度推介 16.familiarity [f?m?l?'?r?t?] n. 亲密关系 17.intimidation [in'timi'dei??n] n. 外在压力 18.conflicts of interests 利益冲突 19.custody of client assets 保管客户资产 20.terminate['t?:m?ne?t] v. (使)终结;(使)结束;解雇 21 eliminate [?'l?m?ne?t] v. 消除;排除 22.solicit [s?'l?s?t] v. 招揽;征求 https://www.wendangku.net/doc/7a14380054.html,work ['netw??k] n. 网络 24.public interest entities 公众利益实体 25.financial interest经济利益 26.immediate family主要近亲属 27.valuation services 评估服务 28. taxation services 税务服务 29. internal audit services内部审计服务 30. IT systems services 信息技术系统服务 31. litigation support services 诉讼支持服务 32. legal services 法律服务 33. recruiting services 招聘服务 34. corporate finance services公司理财服务 35.overdue fee 逾期收费 36. contingent fee 或有收费 37. referral fee 介绍费38.actual or threatened litigation* 诉讼或诉讼威胁 39.successor auditor 后任注册会计师 40.present auditor 现任注册会计师 41.predecessor n. 前任;前辈predecessor auditor 前任注册会计师 42.audit ['??d?t] v. & n. 审计 43.auditor ['??d?t?] n. 审计师;审计人员 44.audit objective审计目标 45. audit evidence['ev?d(?)ns] 审计证据 46 .audit resources[ri'z?:siz] 审计资源 47.audit risk 审计风险 48. inherent risk固有风险 49.control risk 控制风险 50. detection risk 检查风险 财会英语词汇(审计)(2)

审计英语期末考试复习题(已翻译)

期末复习题 一、Answering the following questions: 1、Discuss the relationship between quality control and generally accepted auditing standards. 讨论质量控制与公认审计标准之间的关系。 2、Two types of attestation services provided by CPA firms are audits and reviews. Discuss the similarities and differences between these two types of attestation services. Which type provides the least assurance? 审计与评论是两种由(注册公共)会计事务所提供的认证服务类型。讨论这两种认证服务的相同与不同之处。哪一种类型提供了最小的保证? 3、There are five conditions that must be met before an auditor can issue a standard unqualified report for the audit of a private company. Please discuss each of these five conditions. 审计员在对私人公司的审计发出一个标准,不合格报告前必须满足五种条件/情况。请讨论每一种条件/情况。 4、There are three conditions requiring a departure from an unqualified audit report. Discuss each of these three conditions and state the appropriate audit report for each condition. 违背/违反一个不合格的审计报告有三个条件。讨论每一个条件并陈述每个条件适当的审计。 5、Discuss the three primary requirements for becoming a CPA.

审计英文词汇整理

v1.0 可编辑可修改 1 审计 鉴证 可信赖程度 of financial statements 财务报表审计 procedures 执行商定程序 levels of assurance 高水平保证 编制 可靠性 相关性 skepticism 职业谨慎 客观性 12. professional competence 专业胜任能力 CPA-in-charge 项目经理 engagement letter 业务约定书 audit 连续审计 client 委托人 CPA 更换注册会计师 existing CPA 现任注册会计师 successor CPA 后任注册会计师 preceding CPA前任注册会计师 the audit report 出具审计报告 专家 board of directors 董事会 of the entity‘ s business 了解被审计单位情况 material misstatement risks评估重大错报风险 the nature, timing and extent of the audit procedures 确定审计程序的性质、时间和范围 general knowledge of 初步了解―――的情况 more knowledge of 进一步了解的情况 prior year‘s working papers 以前年度工作底稿 of meeting 会议纪要 risks 经营风险 适当性 estimate 会计估计 representations 管理层声明 concern assumption 持续经营假设 plan 审计计划 audit areas 重点审计领域 错误 舞弊 or additional procedures 修改或追加审计程序 of assets 侵占资产 without substance 虚假交易 pressures 异常压力 suspected noncompliance 涉嫌存在违法行为 重要性 the materiality level 超过重要性水平 the materiality level 接近重要性水平 acceptably low level 可接受水平 overall financial statement level and in related account balances and transaction levels 财务报表层和相关账户、交易层 or omissions 错报或漏报

年度审计报告中的会计及审计英语

年度审计报告中的会计及审计英语

年度审计报告中的会计及审计英语 English for Accounting & Auditing in Annual Repor 主要内容 Contents 年度审计报告框架 Framework of Annual Report 年度审计报告中所应用的相关专业会计及审计英语 Accounting and Audit English in Annual Report 年度审计报告框架 Framework of Annual Report 审计意见Audit opinion 管理层责任Management’s Responsibility for the Financial Statements 注册会计师责任Auditors’ Responsibility 审计意见Auditor’s Opinion

管理层财务报表Management Financial statements 资产负债表Balance Sheet 利润表Income Statements 现金流量表Cash flow statement 财务报表附注Notes to the financial statements 年度审计报告范例-管理层责任(1) Example - Management’s Responsibility(1) 按照中华人民共和国财政部颁布的企业会计准则的规定编制财务报表是贵公司管理层的责任。The Company’s management is responsible for the preparation of these financial statements in accordance with China Accounting Standards for Business Enterprises issued by the Ministry of Finance of the People’s Republic of China. 年度审计报告范例-管理层责任(2) Example - Management’s Responsibility (2)

审计业务常用英语单词

审计业务中常用的128个英文单词 1.audit 审计 2.attestation 鉴证 3.credibility 可信赖程度 4.audit of financial statements 财务报表审计 5.agreed-upon procedures 执行商定程序 6.high levels of assurance 高水平保证 https://www.wendangku.net/doc/7a14380054.html,pilation 编制 8.reliability 可靠性 9.relevance 相关性 10.professional skepticism 职业谨慎 11.objectivity 客观性 12. professional competence 专业胜任能力 13.Senior/CPA-in-charge 项目经理 14.audit engagement letter 业务约定书 15.recurring audit 连续审计 16.the client 委托人 17.change CPA更换注册会计师 18.the existing CPA 现任注册会计师 19.the successor CPA 后任注册会计师 20.the preceding CPA前任注册会计师

21.issue the audit report 出具审计报告 22.expert 专家 23.the board of directors 董事会 24.knowledge of the entity’ s business 了解被审计单位情况 25.assess material misstatement risks评估重大错报风险 26.detemine the nature,timing and extent of the audit procedures 确定审计程序的性质、时间和范围 27.a general knowledge of ——初步了解―――的情况 28.a more knowledge of——进一步了解的情况 29.the prior year‘s working papers 以前年度工作底稿 30.minutes of meeting 会议纪要 31.business risks 经营风险 32.appropriateness适当性 33.accounting estimate 会计估计 34.management representations 管理层声明 35.going concern assumption 持续经营假设 36.audit plan 审计计划 37.significant audit areas 重点审计领域 38.error 错误 39.fraud舞弊 40.modified or additional procedures 修改或追加审计程序 41.misappropriation of assets 侵占资产